At its most basic, a clients trust account is a special bank account where a law firm holds money that belongs to its clients. This is not the firm's money. It is a temporary holding place for funds like retainers, settlement proceeds, or real estate deposits. Think of it as a fiduciary responsibility, a solemn promise to safeguard client funds entirely separate from your own operating cash.

Why Mastering Your Clients Trust Account Is Non-Negotiable

For many lawyers, managing a client trust account feels like walking a tightrope. It is so much more than just bookkeeping; it is the very foundation of ethical practice and your absolute duty to protect what your client has entrusted to you. It is less like a bank account and more like a secure vault where you are temporarily guarding assets that are not yours.

The line between your firm's money and your client's money has to be crystal clear and non-negotiable. Getting this wrong has serious consequences, and unfortunately, it is a mistake that happens more often than you would think. In the high stakes world of law, messing up a client trust account is a recurring nightmare for firms of all sizes.

In fact, according to recent analyses, trust account mismanagement is behind a staggering 15% of all disciplinary actions against lawyers. You can get more insights on this from legal compliance experts at accountantslawlab.com. That number is not just a statistic; it represents a major weak spot for even the most well meaning attorneys.

The Foundation of Client Confidence

How you handle a client's trust account speaks volumes about your firm's integrity. When clients hand over their money for a retainer or wait for you to disburse a settlement, they are placing an incredible amount of faith in your professionalism. Managing those funds meticulously reinforces that trust and helps build a strong, transparent relationship from day one.

On the flip side, even a small error can shatter that confidence in an instant. A simple slip up, like accidentally paying a firm invoice from the trust account, can look terrible and trigger tough questions from clients and, even worse, the state bar.

At its core, a clients trust account is a physical manifestation of your fiduciary duty. It is where your ethical obligations meet practical, day to day financial management.

Turning Anxiety into Assurance

This guide is your roadmap to managing your client trust account with confidence. We are going to break down every critical piece, starting with the basic principles and moving all the way to concrete, actionable steps you can take today.

Our goal is to help you:

- Understand your ethical duties and what they actually look like in practice.

- Master the accounting procedures needed for perfect, audit proof records.

- Identify and avoid the common pitfalls that get lawyers into hot water.

- Use modern tools to make compliance and client communication easier.

By the time you are done with this guide, you will have the knowledge and the framework to turn that nagging trust account anxiety into the solid assurance that your firm is meeting the highest ethical standards.

Understanding the Core Principles of Trust Accounting

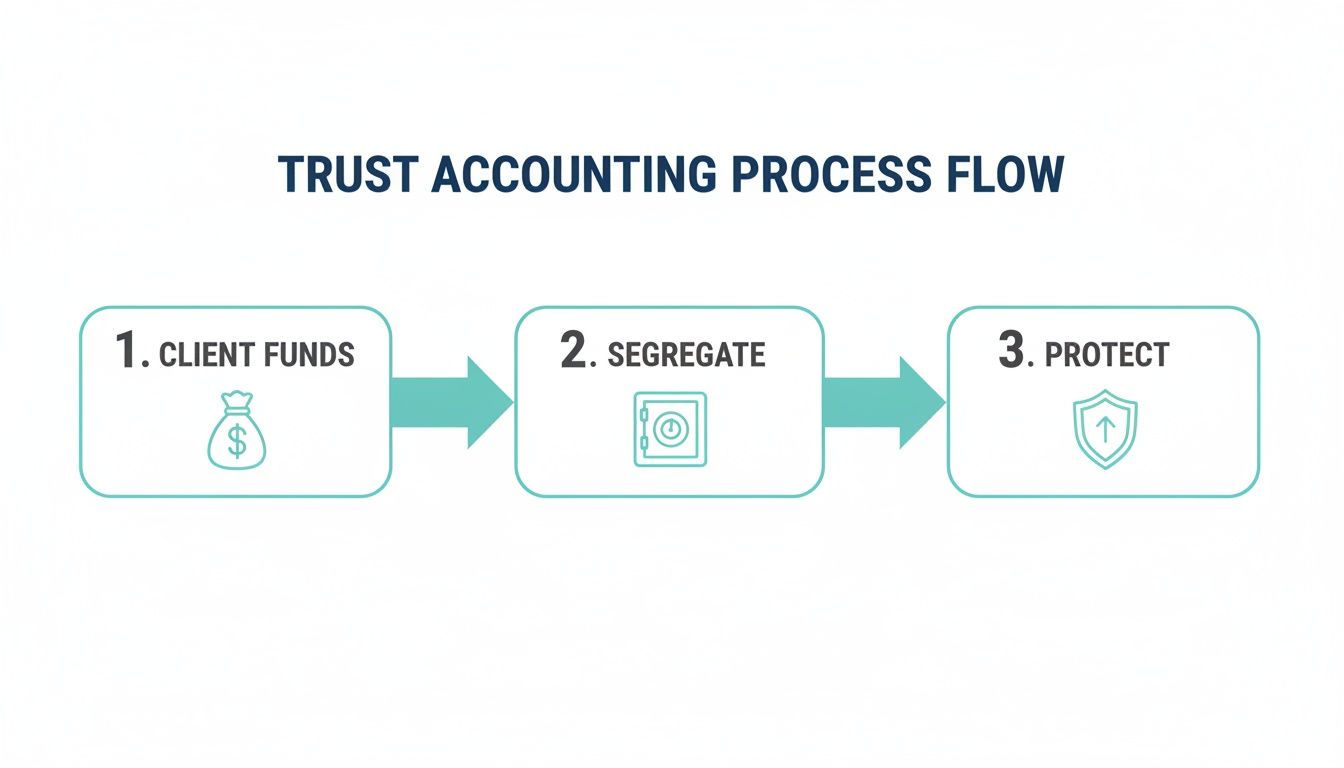

Let's start with the one idea that underpins everything in trust accounting: it’s not your money. When you hold a client's funds, you are their fiduciary, a trusted guardian of their property. This is not just a nice sounding ethical concept; it is the absolute, non-negotiable foundation of every rule and regulation governing a clients trust account.

Think of it this way: you are essentially a professional valet for your client’s money. You would not take their car for a joyride or use it to run errands, right? You park it safely, protect it, and hand the keys back when they are ready. A trust account works exactly the same way, ensuring every dollar is protected, meticulously accounted for, and used only as directed.

This separation between your firm's money and your client's money must be a firewall. Any hint of mixing them, a practice called commingling, can lead to severe disciplinary action.

The Two Main Types of Trust Accounts

Not all client funds are created equal, and how you handle them depends on the amount and how long you will be holding onto them. This is why there are two main types of trust accounts. They share the same goal of safeguarding client money, but they operate quite differently.

First, you have the IOLTA account, which stands for Interest on Lawyers' Trust Accounts. This is the workhorse for most firms. It is a pooled account where you can hold funds from multiple clients at once. IOLTAs are perfect for smaller sums or funds you will only have for a short time, like retainers or small settlement deposits. The tiny bit of interest generated from these pooled funds is not kept by you or the client. Instead, it is sent to state approved programs that fund civil legal aid for those who cannot afford it.

The second option is an individual trust account. You open this type of account for a single client to hold only their funds. This is the right choice when a client gives you a very large sum of money or when the funds will sit for a long time. In this case, the interest earned is substantial enough to be paid directly to that specific client.

The key distinction is simple: an IOLTA account pools small or short-term funds from many clients for a collective public benefit, while an individual account segregates a large or long-term sum for a single client's benefit.

Getting this choice right is your first step toward proper trust management. You would not use an IOLTA for a massive, multi year settlement, nor would you open an individual account for a small retainer. Using the wrong one can cause serious compliance headaches down the road.

IOLTA vs. Individual Trust Account at a Glance

To make the decision even clearer, it helps to see the differences side by side. Knowing when to use each type of clients trust account is fundamental to staying on the right side of state bar rules.

This table breaks down the scenarios for each.

| Feature | IOLTA (Pooled Account) | Individual Trust Account |

|---|---|---|

| Best For | Smaller amounts of money or funds held for a short duration. | Large sums of money or funds held for an extended period. |

| Interest | Interest is pooled and remitted to state-run legal aid programs. | Interest is paid directly to the individual client. |

| Structure | Holds funds from multiple clients in a single, commingled account. | A separate account is established for one specific client's funds. |

| Example Use | A $2,500 retainer from a client for a new case. | A $500,000 settlement that needs to be held for several months. |

No matter which account you use, remember the golden rule: never commingle client funds with the firm’s operating funds. The money in a trust account is not your firm’s asset. You cannot use it to pay salaries, cover the office rent, or even pay for a bank fee on the trust account itself. This strict separation is the very bedrock of your ethical duty as a lawyer.

Mastering Recordkeeping and Reconciliation

Let's move from theory to practice. At the end of the day, properly managing a client trust account comes down to one thing: meticulous daily habits. Flawless recordkeeping is not just a "best practice", it is a non-negotiable part of your fiduciary duty. Without it, you are flying blind, risking serious ethical violations and shattering the trust you have worked so hard to build.

Great trust accounting really hinges on two things: diligent recordkeeping and a critical process called reconciliation. To stay compliant and accurate, you have to regularly master bank account reconciliation. This is not just about balancing a checkbook; it is about being able to prove, at any moment, that every single dollar is exactly where it is supposed to be.

The entire process is built on a simple, foundational principle.

As you can see, the journey of your client's funds is all about strict segregation and unwavering protection. That is why precise documentation at every single stage is so important.

The Essential Records You Must Maintain

Every state bar has specific, detailed requirements for the records a law firm must keep for a client trust account. And while the rules might vary a bit by jurisdiction, a core set of documents forms the backbone of any compliant system. Lapses here are one of the fastest ways to land in hot water with the bar.

Make no mistake, recordkeeping failures are not minor oversights. In fact, they contribute to a shocking 25% of annual lawyer disciplinary actions, according to American Bar Association data. Improper tracking is a top violation, and it is a huge red flag for auditors.

To keep your practice safe and stay audit ready, you must maintain these three records at all times:

- A Trust Receipts Journal: Think of this as a chronological log of every penny that comes into the trust account. Each entry needs to detail the date, who the money came from (client name), the amount, and why you received it.

- A Trust Disbursements Journal: This is the flip side, a detailed log of all money paid out of the account. It should include the date, check number, who was paid, the amount, and a crystal clear description of the payment's purpose.

- Individual Client Ledgers: Every single client with funds in your trust account must have their own separate ledger. This document tracks all the activity for that client, showing every deposit, every withdrawal, and the current running balance you hold for them.

These three documents are the bedrock of trust accounting. They create a complete, transparent trail showing where the money came from, where it went, and who it belongs to. Most states require you to hang onto these records for a long time, often five to seven years after a case closes.

Demystifying the Three-Way Reconciliation

The absolute cornerstone of managing a trust account is the three-way reconciliation. This is a monthly checkup that proves your internal records are in perfect sync with the bank's records. It is called "three-way" for a simple reason: you have to demonstrate that three different totals match down to the last cent.

I like to think of it as a three legged stool. If one leg is even slightly off, the whole thing becomes unstable and collapses.

The goal of a three-way reconciliation is to verify that the trust bank account balance, the trust account checkbook register, and the sum of all individual client ledger balances are identical. A perfect match is the only acceptable outcome.

If those numbers do not align, it is an immediate red flag that something is wrong. It could be a simple typo, or it could be a sign of something much more serious, like commingling funds or an accidental overdraft on a client's balance. This monthly process is your critical early warning system.

Here is a quick breakdown of how it works:

- Balance the Bank Statement: Start with your monthly statement from the bank. Adjust its ending balance by accounting for any outstanding checks or deposits that have not cleared yet. This gives you your adjusted bank balance.

- Verify Your Checkbook Register: Next, go through your firm’s internal checkbook register or cash journal. Compare it line by line against the bank statement, ticking off every transaction that has cleared. The final balance here should match your adjusted bank balance from step one.

- Sum the Client Ledgers: Finally, add up the ending balances from every single one of your individual client ledgers. This grand total must equal the balances from the first two steps.

Performing this check religiously every month is your single best defense against errors and is a key requirement to be prepared for an audit. This level of diligence also makes client communication easier; having flawless records is the first step toward secure file sharing.

Avoiding Common Trust Accounting Pitfalls

Even the most careful law firms can trip up on trust accounting. These mistakes rarely happen because of bad intentions; more often, they are the result of a simple oversight, a lack of solid internal processes, or just not fully grasping the strict rules that govern a client's trust account. Messing this up can lead to serious ethical trouble, so understanding the common pitfalls is the first step to avoiding them completely.

The goal is to build a fortress of compliance around your client funds. That starts by finding the weak spots where mistakes are most likely to sneak in. Think of it as preventative maintenance for your firm’s ethical health. A small investment in your process now can prevent a massive headache later on.

The Cardinal Sin: Commingling Funds

By far, the most common and dangerous mistake is commingling funds. This is what happens when you mix your law firm's operating money with client trust funds in the same bank account. It sounds easy enough to avoid, but it can happen in subtle ways that catch even seasoned lawyers off guard.

For example, paying a firm expense, like a vendor invoice or even a small bank service charge, directly from the trust account is a classic example of commingling. Another frequent error is depositing an earned fee straight into the trust account instead of your firm's operating account. Actions like these blur the sacred line between your money and your client’s money.

Commingling client funds remains the number one trust accounting mistake for law firms everywhere. The Florida Bar, for instance, explicitly requires lawyers to hold client property 'separate from the lawyer’s own property,' yet violations are still surprisingly common.

The rule is absolute: a client's trust account is a sanctuary for client money only. The one exception, allowed in most states, is keeping a small amount of firm funds in the account specifically to cover bank maintenance fees.

Allowing a Client Ledger to Go Negative

A client’s individual ledger balance can never, ever be negative. A negative balance means you have spent more money for that client than they gave you to hold. But what it really means is that you have accidentally used another client's funds to cover the first client's expenses, a serious breach of your fiduciary duty.

This often happens because of simple clerical errors or bad timing. You might cut a check for a court filing fee before the client's retainer check has actually cleared the bank. If that retainer check bounces, the client's ledger immediately plunges into the red.

To stop this from ever happening, you need a strict policy in place:

- Verify Funds: Always confirm a client's deposit has fully cleared and is available before you spend any of it on their behalf.

- Regular Reconciliation: Perform your three-way reconciliation every single month. This is your safety net for catching a negative balance before it spirals into a bigger problem.

- Real-Time Tracking: Use accounting software that gives you a live, up to the minute view of each client's ledger balance.

Improper Disbursements and Poor Communication

Two other pitfalls often go hand in hand: paying out funds incorrectly and failing to keep clients in the loop. An improper disbursement could mean paying the wrong person, paying an amount before it is authorized, or pulling your earned fees before you have properly invoiced the client.

At the same time, poor communication can turn a simple transaction into a source of suspicion. When you receive settlement funds or a retainer, you have to tell the client right away. Leaving them in the dark about the status of their money erodes trust and is a common reason clients file complaints with the state bar.

To steer clear of these issues, your firm needs clear, documented procedures for every single transaction. Strong internal systems, often supported by legal case management software, are critical for tracking every step and maintaining a clear audit trail.

Proactive Solutions to Strengthen Controls:

- Written Disbursement Authorization: Get written approval from the client before making any significant payments from their trust funds. No exceptions.

- Automated Client Notifications: Set up your systems to send automatic alerts to clients when their funds are received or paid out.

- Invoice Before Transfer: Never, ever move earned fees from the trust account to your operating account until a detailed invoice has been sent to the client.

By understanding these common traps and putting clear, proactive solutions in place, you can protect your firm, stay compliant, and honor the trust your clients have placed in you.

Improving Trust Account Communication with Clients

Running a client trust account properly is about more than just perfect bookkeeping. It is about clear, constant communication that builds confidence and puts your clients at ease. Let's be honest, nothing makes a client more anxious than feeling left in the dark about their money. That anxiety is what leads to the non-stop phone calls asking, "Where are my funds?"

The real key to a solid attorney client relationship is answering that question before they even have to ask. When clients feel looped in on the status of their funds, they feel secure. This is not just about good customer service, it is a core part of your fiduciary duty.

Communicating effectively about trust funds cements your firm’s reputation for integrity. It demonstrates that you respect their assets and are committed to keeping them informed every step of the way. Handled correctly, this turns a major potential point of friction into an opportunity to build even deeper trust.

Bridging the Gap Between Accounting and Communication

Your trust accounting software is the engine for managing the numbers, but it was never built for client facing conversations. That is where a dedicated communication tool comes in, acting as a bridge between your diligent back office work and a transparent client experience.

A secure client portal complements your accounting system; it does not replace it. Think of your accounting software as the bank vault, securely holding and tracking the money. The client portal is the secure viewing window. It gives clients a clear look at relevant information and a way to talk to you about it, all without handing them the keys to your sensitive accounting systems.

A dedicated communication portal lets you provide crucial updates on fund status, share documents, and keep a clear record of all interactions. This strengthens both your client relationships and your internal documentation.

This separation is crucial. Your accounting system handles the heavy lifting of compliance and reconciliation. A portal like CasePulse manages the client facing side of the conversation, making sure every communication is secure, documented, and professional.

Proactively Answering the Big Questions

A client portal provides a central, secure hub for sharing important financial documents and updates. This proactive approach helps manage client expectations and dramatically cuts down on the time you spend fielding calls from worried clients.

Here’s how a portal can strengthen your trust account communication:

- Secure Document Sharing: Instead of relying on insecure email, you can securely upload and share settlement statements or disbursement authorizations. This protects sensitive financial data.

- Real-Time Updates: Keep clients in the loop with timely notifications. For example, you can let them know the moment a settlement check has been received and deposited.

- Clear Communication Record: Every message and update is logged directly within the client's case file. This creates a clean, chronological paper trail that is invaluable for audit readiness and heading off potential disputes.

By using the right tools, communication shifts from a reactive chore to a proactive strategy. To learn more about what to look for, you can read about how to choose the best client portal software for your firm's specific needs. A good system provides peace of mind for your clients while reinforcing the meticulous care you take in managing their funds.

How to Prepare for a Trust Account Audit

The single best piece of advice for facing a state bar audit is to run your firm as if one could happen tomorrow. This simple shift in mindset changes everything. Instead of reacting to an audit notice with panic, you treat it like a routine checkup. At its core, an audit is just a review to make sure you are properly managing your clients trust account.

When your records are consistently immaculate, an audit notice is a minor blip on the radar, not a full blown crisis. The secret is to weave audit ready habits into your firm's daily DNA, making compliance a constant, not a last minute scramble.

What Auditors Are Looking For

State bar auditors are trained to look for specific red flags that point to the mishandling of client funds. They follow a very specific paper trail to make sure every penny is accounted for and that your firm is playing by the rules. Knowing what they focus on is half the battle.

Their primary mission is to confirm two things: that client funds are kept completely separate from your firm's money and that every single transaction is accurately recorded and properly authorized. Any hint of sloppy bookkeeping or commingling is guaranteed to invite a much deeper look from the state bar.

Think of an audit as a test of your systems. Auditors want to see a clear, logical, and complete paper trail that proves you are upholding your fiduciary duty to every client.

Key Documents Auditors Will Request

When the auditors arrive, they will have a shopping list of records they need to see. Having these documents organized, complete, and ready to go is the first step to a smooth and painless audit. It is smart to keep these files updated and reviewed regularly, not just when an audit is on the horizon.

Get ready to hand over the following:

- Complete Bank Records: This means every single bank statement for your trust account covering the audit period, plus copies of all deposited checks and front and back images of all cleared checks.

- Reconciliation Reports: Auditors will demand to see your monthly three-way reconciliations. These reports are the concrete proof that you are actively balancing and monitoring the account.

- Client Ledgers: You will need to produce an individual ledger for every client who had money in the trust account during the audit window. Crucially, the sum of all these individual client balances must perfectly match your reconciled bank balance.

- Cash Journals: Both your trust receipts journal (money in) and your disbursements journal (money out) will be reviewed to trace the complete lifecycle of funds moving through the account.

Some firms are now using new AI powered tools for transforming regulatory compliance, which can help automate checks and bolster a firm's ability to meet these tough audit requirements.

Your Internal Audit Checklist

To truly stay audit ready, you need to audit yourself. Conducting your own internal reviews on a regular schedule helps you find and fix small mistakes before they balloon into serious compliance violations. Treat it like a dress rehearsal for the main event.

- Perform Monthly Reconciliations: This is absolutely non-negotiable. The three-way reconciliation is the most critical internal control you have.

- Review Client Ledgers: Every quarter, pull a random sample of client ledgers. Check them for accuracy and, most importantly, confirm that no client balance has ever dropped into the negative.

- Check for Stale Funds: Actively look for client money that has been sitting untouched in the account for too long. Find out why it is still there and take action.

- Verify All Transactions: Make sure every single payment out of the trust account is backed by clear documentation, like a client signed invoice or a settlement statement.

Common Questions About Client Trust Accounts

Even with the best intentions, managing a client trust account can feel like walking a tightrope. A lot of questions pop up in the day to day running of a practice. Let's tackle some of the most common ones with straightforward, practical answers.

How Should I Handle a Client's Retainer?

Think of a retainer as money that is on hold. It is not yours yet. The moment you receive it, that retainer must go directly into your IOLTA or individual client trust account. It belongs to the client until you have actually done the work, sent them an invoice, and officially "earned" it.

Only then can you transfer the exact amount of your earned fees from the trust account over to your firm’s operating account. Whatever you do, never deposit a retainer straight into your business account. That is the textbook definition of commingling funds, a serious ethical breach that can land you in hot water.

What Do I Do If I Find a Mistake in My Records?

Okay, do not panic. Mistakes happen. The key is how you respond. The second you spot an error, maybe you recorded a deposit incorrectly or paid an expense from the wrong account, you need to act.

First, document everything. Write down exactly what happened, when you found it, and how it occurred. Then, fix it immediately. If client funds were accidentally used, this usually means putting your own money back into the trust account to make it whole again. Finally, document the fix. Quick, transparent action shows you are acting in good faith, which makes all the difference if a bar auditor ever comes knocking.

The most critical response to a trust accounting error is immediate correction and complete documentation. Ignoring a mistake, even a small one, is a guaranteed way to turn a minor issue into a major disciplinary problem.

Can Clients Make Electronic Payments into the Trust Account?

Absolutely, but you have to be careful. While electronic payments are convenient, the system you use must be set up correctly to direct those funds straight into the client trust account, not your operating account.

Here is the critical part: any credit card or processing fees must be paid from your firm's operating account. You can never let those fees get deducted from the client's funds in trust. Many modern payment processors built for law firms, like LawPay or Clio Payments, are designed to handle this automatically, ensuring you stay compliant with the strict rules on segregating funds.