A managing partner usually starts looking at legal fee loans at the same moment pressure shows up from three directions at once. Case costs are climbing. Clients want help now, not after they've figured out how to fund a retainer. Staff is spending too much time chasing partial payments, answering billing questions, and deciding which matters can move forward before money is in the door.

That pressure is common in plaintiff work, especially when a case needs experts, depositions, medical records, filing fees, and other out of pocket spending before any recovery exists. The funding question isn't abstract. It affects intake, case selection, staffing, collections, and client satisfaction.

Legal fee loans are part of the broader legal finance sector, but they are not the same thing as every other funding product your team may hear about. A 2014 law review article on alternative litigation finance distinguishes lawyer lending from consumer legal funding and commercial litigation investment, and describes lawyer lending as loans to plaintiffs' lawyers and firms for case costs and litigation expenses. That distinction matters because firms often mix together very different products when they discuss “litigation finance.”

For a law firm, the question isn't whether financing exists. It does. The question is whether a specific legal fee loan option helps the firm solve a payment problem without creating a client relationship problem, a compliance problem, or a reputation problem.

Introduction Navigating Case Costs and Client Funding

In a plaintiff firm, money rarely arrives on the same schedule as work. You may need to order records this week, retain an expert next week, and advance filing costs before the case has generated a dollar. At the same time, a prospective client may be able to afford the case in the long run but not in one large payment today.

That's where firms start considering legal fee loans. Not as a cure all, and not as a substitute for sound case economics, but as one tool that can bridge a timing gap between the client's need for representation and the client's ability to pay up front.

What legal fee loans are not

One of the most useful starting points is to separate client side financing from other legal finance products.

- Not lawyer lending: Some financing products are aimed at the firm or the lawyer for case preparation and expenses.

- Not consumer legal funding: Other products advance money to plaintiffs for personal use and are repaid from a case outcome.

- Not litigation investment: Commercial litigation finance is its own category with a different risk structure and purpose.

A lot of internal confusion disappears once your intake and finance teams stop using one label for all three.

Firms make bad policy when they treat every funding product as if it has the same borrower, the same repayment source, and the same ethical risk.

Why firms care about them

From the firm's perspective, legal fee loans come up when any of these are true:

- A good client can't fund a retainer immediately

- The firm doesn't want to become a consumer lender

- Collections work is eating staff time

- The firm wants payment certainty before substantial work begins

In practice, the issue is often less about theory and more about workflow. If a financing option gets the invoice paid promptly, the file opens faster, accounting spends less time carrying receivables, and lawyers can focus on legal work instead of payment triage.

Still, this only works when the firm understands the product well enough to explain its role clearly and stay inside ethical lines. Clients need representation, not pressure. Firms need payment, not avoidable complaints.

Understanding How Legal Fee Loans Work

At the simplest level, a legal fee loan is usually an unsecured personal loan the client uses to pay the lawyer. The client borrows from a lender. The firm gets paid. The client repays the lender over time.

A useful analogy is a home improvement loan. The homeowner borrows from a lender to pay the contractor now, then repays the lender in installments. The contractor is not extending credit. The contractor is getting paid for the job.

According to SoFi's overview of loans for legal fees, these loans are typically unsecured personal loans used to pay a lawyer up front, with repayment in fixed monthly installments over terms that commonly range from about 2 to 7 years. Because the loan is unsecured, approval depends heavily on repayment capacity and credit quality, and longer terms generally lower monthly payments while increasing total interest cost.

The workflow from the firm's seat

Most firms encounter the process in a sequence like this:

The client needs financing

The matter is viable, but the client can't or won't pay the full amount up front.The client applies with a lender

The application is with the third party lender, not with the law firm.The lender underwrites the borrower

The lender looks at the client's ability to repay, credit profile, and related financial factors.Funds are disbursed

Depending on the program, money may be delivered to the firm to satisfy the legal invoice.The firm performs the work

The representation proceeds under the engagement terms.The client repays the lender

The monthly payment obligation runs between the client and the lender.

What this changes operationally

The core operational shift is simple. Your firm stops carrying the payment risk associated with installment billing. Instead of waiting on monthly checks from the client, the firm receives payment tied to the lender's funding process.

That can be useful, but only if your staff explains one point with total clarity: the loan is not a payment plan with the law firm. It is a separate credit obligation. If clients confuse those two arrangements, complaints usually follow.

Practical rule: Intake staff should explain the transaction in one sentence. “If you use financing, you'll repay the lender, not the firm.”

Where firms get tripped up

Problems usually come from fuzzy handoffs.

- Blurred roles: The client thinks the firm approved the loan.

- Incomplete explanations: Nobody explains that monthly payments continue even if the client is unhappy with the lender.

- Wrong account handling: Staff doesn't coordinate properly with trust and operating account rules.

- Overpromising approval: A lawyer or case manager talks as if funding is guaranteed.

The firms that handle this best build a short, repeatable script for intake, billing, and attorney follow up. They don't improvise.

Decoding Fee Structures and Potential Costs

If your firm is going to discuss legal fee loans with clients, the most important discipline is cost literacy. Not sales language. Not convenience language. Cost literacy.

The client may focus on the monthly payment because that's what feels immediate. The firm should care about the full repayment burden, the disclosures, and whether the pricing is being described in a way an ordinary borrower can understand.

What to review in the loan terms

When a client shows your office a financing offer, these are the parts worth slowing down for:

- APR: This is the most useful single measure for comparing borrowing cost across options.

- Repayment term: Lower monthly payments can still mean a more expensive loan overall if the term stretches out.

- Fees: A loan can look manageable at first glance and still carry cost in ways the client didn't expect.

- Disclosure language: If the pricing is hard to follow, assume the client will misunderstand it.

The regulatory backdrop matters here. The National Consumer Law Center's 2024 report on state installment loan protections reported that for a $2,000 two year installment loan, 43 states and the District of Columbia cap rates at a median of 34% APR, and for a $500 six month installment loan, 45 states and DC cap rates at a median of 39.5% APR. The same report notes that some lenders can present costs in misleading ways, including an example framed as 24% per year plus 7/10ths of a percent per day instead of 279% APR.

Why this matters in a law office

A client who doesn't understand the financing cost may later decide the firm steered them into a bad arrangement, even if the legal work was solid. That risk is practical, not theoretical.

For plaintiff firms, it also intersects with settlement expectations. Clients often think in net terms. If they're already trying to estimate what they might receive at the end of a case, confusion about legal fees, expenses, and financing cost can compound quickly. A plain English explanation of how lawyers' fees may affect a settlement can help frame that broader conversation.

What works and what doesn't

A few habits help.

| Review approach | Result |

|---|---|

| Client sees only monthly payment | High risk of misunderstanding |

| Client reviews APR, term, and fee language | Better informed consent |

| Firm uses a neutral explanation | Lower pressure, cleaner expectations |

| Staff minimizes the cost discussion | Higher chance of later conflict |

What doesn't work is saying, “It's affordable,” or “This is the easiest route.” A law firm shouldn't characterize consumer credit that way. The better approach is narrower: identify the structure, point the client to the disclosure, and encourage review before signing.

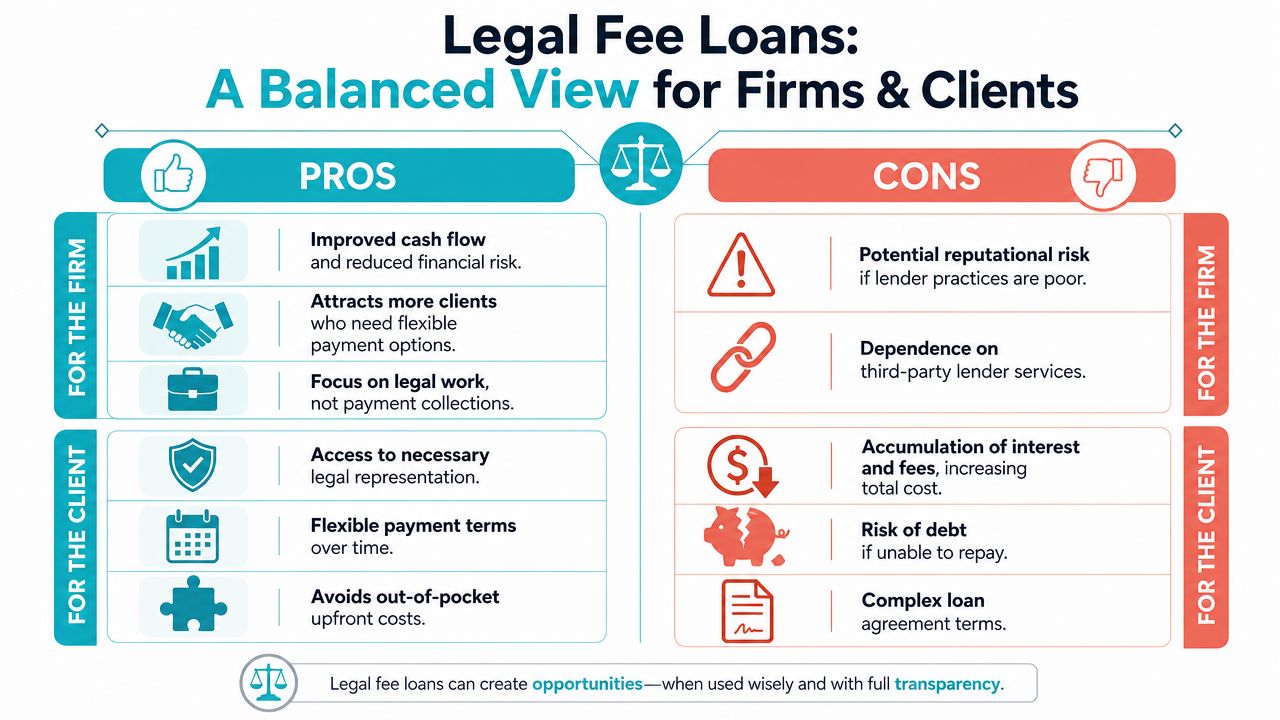

The Pros and Cons for Your Firm and Client

From the firm's perspective, the attraction is obvious. Third party financing can clean up the payment side of the engagement. From the client's perspective, the attraction is also obvious. It can create a path to representation when paying all at once isn't realistic.

Those two benefits are real, but they don't eliminate the tension between access and cost.

What firms gain

The strongest operational case for legal fee loans is on cash flow and collections. LawPay's legal industry guidance on loans for legal fees explains that third party legal fee financing shifts cash flow timing and collection risk away from the firm because the firm receives the invoiced amount up front while the lender handles repayment from the client. It also notes that compliant programs must align with ABA and IOLTA rules.

In day to day practice, that can mean:

- Cleaner receivables: The firm isn't carrying the same level of installment risk on its own books.

- Less collection friction: Staff spends less time on partial payments and overdue balances.

- More predictable intake conversion: A client who can't pay immediately may still move forward.

- Lower accounting drag: Reconciliation is usually simpler than managing long running in house payment arrangements.

What clients gain

For clients, the upside is straightforward.

- Access to counsel: They may be able to retain the firm without producing the entire amount up front.

- Structured repayment: Fixed monthly payments can be easier to plan around than one lump sum.

- Faster start to representation: Work can begin without waiting for the client to assemble funds.

Where the downside lives

The cost burden sits primarily with the client. That's the central trade off. The firm benefits from cleaner cash flow. The client takes on a debt obligation that may substantially increase the total amount paid over time.

If the financing solves your collection problem by creating a client regret problem, it hasn't solved much.

There are firm side downsides too.

- Reputational spillover: Clients often blame the law firm for a lender's poor communication or aggressive servicing.

- Dependency risk: If your intake process relies too heavily on one financing partner, service problems become your problems.

- Ethical exposure: Staff can cross a line if they pressure clients, present one lender as the only option, or speak too confidently about loan suitability.

The practical balancing test

When firms evaluate whether legal fee loans belong in the payment mix, I usually suggest a simple internal question set:

| Question | If yes | If no |

|---|---|---|

| Does this help a qualified client start representation? | Consider offering the option | Don't add complexity |

| Can staff explain the arrangement neutrally? | Lower relationship risk | Pause rollout |

| Are terms transparent enough for a client to understand? | Safer to discuss | High complaint risk |

| Can your firm support compliance and account handling correctly? | Operational fit | Don't proceed yet |

Legal fee loans work best as one option among several. They work worst when the firm treats them as the default answer to every payment problem.

How Law Firms Should Evaluate Lenders

The quality of the lender matters as much as the existence of financing. If your firm refers clients to a lender with confusing disclosures, weak service, or poor legal workflow, your team will end up absorbing the fallout.

That's why lender review should be a formal process, not an informal preference held by whoever handles intake.

The non negotiables

A lender is worth considering only if it clears these basic checks:

- Transparent disclosures: The borrower should be able to identify the APR, repayment schedule, and fees without hunting through dense language.

- Clear role separation: The process should make it obvious that the client is borrowing from the lender, not from your firm.

- Reliable funding mechanics: Your accounting team needs to know how funds move and where they should be posted.

- Consumer compliant posture: The lender's materials, servicing, and disclosures should fit the legal and regulatory environment where your clients are located.

That last point needs real attention. If your internal payment controls are already weak, adding financing can magnify the problem. Before you refer anyone to a lender, make sure your team has a clean understanding of client trust account handling, because account errors can create larger problems than payment delays ever did.

A due diligence framework

I'd review a lender in four passes.

First pass through the client experience

Have someone at the firm walk the application and disclosure flow as if they were a client. Don't look at it as a lawyer first. Look at it as a borrower.

Ask:

- Is the loan clearly described as third party credit?

- Can a client understand when repayment begins?

- Are there any phrases that sound deceptively easy or overly promotional?

- Does the process create confusion about the firm's role?

Second pass through operations

Your billing and accounting teams should map the life of a funded invoice.

- How is the invoice satisfied?

- What happens if the matter changes scope?

- How are refunds handled if required?

- Which account receives funds under the applicable rules?

Third pass through ethics and governance

The firm needs written internal boundaries.

- Who may discuss financing with clients

- What scripts they may use

- What they must never say

- When lawyers need to step in

- Whether the firm offers more than one payment path

Governance test: If a client later says, “Your firm pushed me into this loan,” you want a documented process that shows the opposite.

Fourth pass through reputation

Look for signs of friction, not just signs of approval. You're not trying to prove a lender is perfect. You're trying to identify whether the lender creates recurring client confusion.

What firms often overlook

The most overlooked issue is service after funding. Approval is only the front end. The complete client experience often turns on billing questions, missed payment questions, and general communication quality once the loan is live.

A lender can look polished in intake and still create headaches later. Ask who handles borrower support, how disputes are routed, and what your staff should say when clients call the firm about lender issues.

Comparing Alternatives to Legal Fee Loans

Legal fee loans aren't the only way to solve a payment problem. In many firms, they shouldn't be the first option reviewed. The better approach is to compare them with the other methods your firm can realistically manage, then decide which method fits the client, the case, and the firm's tolerance for risk.

Financing options at a glance

| Financing Method | Who Bears Risk | Firm Cash Flow Impact | Client Cost |

|---|---|---|---|

| Traditional retainer | Client | Strong up front | Immediate out of pocket burden |

| Contingency arrangement | Firm | Delayed until recovery | No up front fee, but tied to outcome and fee structure |

| Firm managed payment plan | Firm | Slower and less predictable | May avoid third party borrowing costs, but depends on firm terms |

| Legal fee loan | Client and lender relationship on repayment, with collection burden shifted away from firm | Up front payment if funded | Interest and fees can increase total cost |

When each option fits

A traditional retainer is still the cleanest answer when the client can pay it without stress. It keeps the relationship simple.

Contingency works when the matter and firm model support it. But many matters don't fit contingency economics, and many costs still need to be funded along the way.

A firm managed payment plan gives the firm control, but it also leaves the firm holding collection risk and administrative burden. Many firms underestimate how much staff time that consumes.

Legal fee loans can make sense when the client needs financing and the firm wants to avoid becoming the collector. They can also sit alongside card acceptance, which is often part of a broader payment policy. If your firm is reviewing payment flexibility generally, it helps to compare financing with whether attorneys accept credit cards and how that changes both client convenience and back office handling.

What usually works in practice

The strongest payment systems are tiered, not one dimensional.

- First option: If the client can pay the retainer cleanly, keep it simple.

- Second option: If the matter fits contingency, evaluate that structure on its own economics.

- Third option: If the client can pay over time and the firm is willing to carry that burden, use a payment plan.

- Fourth option: If the firm wants immediate payment and the client wants installment financing, legal fee loans may fit.

This is a policy choice as much as a billing choice. Firms that do this well decide in advance which case types, fee structures, and client situations qualify for each path. Firms that do it poorly decide in the hallway after a rushed consultation.

Key Questions PI Firms Ask About Legal Fee Loans

Can a PI firm discuss legal fee loans with clients?

Yes, but the discussion should stay neutral and factual. The firm can explain that financing exists, how the basic structure works, and where the client can review terms. The firm shouldn't pressure the client, guarantee approval, or speak as if the firm is giving financial advice.

Can a firm require a client to use a specific lender?

That's where firms need to be careful. As a practical matter, requiring one lender can create both perception and ethics issues. A better approach is to present financing as one available payment path and keep the client's consent informed and voluntary.

Does the firm need a written policy?

Absolutely. If your intake team handles these conversations ad hoc, inconsistency will show up fast. A written policy should cover who may mention financing, what they may say, how loan related questions are escalated, and how funds are handled once received.

Put the financing script in writing. If it lives only in staff memory, it will change from person to person.

How do legal fee loans interact with settlement expectations?

Indirectly, but meaningfully. Clients often think in terms of what they'll “end up with.” If they have legal fees, case expenses, and a financing obligation in the picture, they need plain communication early. The firm doesn't need to calculate every future scenario to explain the obvious point that borrowed money has a cost.

What's the biggest mistake firms make?

Treating legal fee loans as a sales tool instead of a payment option.

When firms stay disciplined, legal fee loans can reduce collection work, improve cash flow timing, and help some clients start representation sooner. When firms get loose with the explanation, the same product can create confusion, resentment, and complaints that linger long after the matter closes.

The firms that handle this best do three things well. They keep the explanation neutral. They vet lenders carefully. They give clients more than one payment path whenever possible.

CasePulse helps plaintiff firms improve the client side of payment conversations and case communication after engagement begins. With CasePulse, firms can give clients a secure portal to check status, message the team, share files, and complete forms without forcing staff to work outside their case management system. If your firm is tightening intake, reducing call volume, and trying to create clearer client expectations from day one, CasePulse is worth a look.