A managing partner usually doesn't call a meeting because a disclosure statement went well. The meeting happens when something small turns expensive. A client says they didn't understand a fee, a buyer claims a defect was never mentioned, or opposing counsel moves to exclude information that should have been disclosed earlier. The work then shifts from serving the client to reconstructing what was said, when it was sent, and whether anyone can prove receipt.

That's why the question what is a disclosure statement matters far beyond legal definitions. In practice, it sits at the intersection of communication, compliance, and operational discipline. Firms that treat disclosures as one more form often create avoidable disputes. Firms that treat them as part of a controlled workflow usually protect both the client relationship and the record.

The Hidden Risks of Miscommunication

A common pattern in firms looks like this. The legal work is sound, the underlying result is acceptable, and the problem starts afterward because the client or counterparty says, “That's not what I thought I was agreeing to.”

It might be a settlement where the client focused on the gross amount and never fully understood offsets, liens, timing, or fee treatment. It might be a property matter where a party says a material issue should have been flagged in writing before signatures. It might be litigation support where a missing or late disclosure weakens a case that was otherwise workable.

The damage isn't abstract. Staff stop what they're doing to search email chains. Partners get pulled into cleanup. Clients lose confidence because they experience the dispute as a failure of honesty, even when the actual failure was a failure of process.

The firms that struggle most with disclosure issues usually don't have a knowledge problem. They have a delivery and tracking problem.

That distinction matters. Most lawyers understand they should communicate material facts. The breakdown happens when no one has a consistent method for gathering the right information, presenting it clearly, confirming delivery, and documenting the client's acknowledgment.

Client expectation management lives in the same lane. If your intake, engagement, document delivery, and follow-up process leave room for ambiguity, disputes tend to appear later when the facts are harder to reconstruct. That's why disciplined disclosure practices belong alongside broader client expectation management, not in a separate compliance bucket.

Where firms usually slip

- Too late: The disclosure arrives after the practical decision has already been made.

- Too vague: The language stays general when the matter requires specifics.

- Too scattered: Key facts are split across calls, emails, attachments, and portal messages with no single authoritative record.

- Too informal: Staff rely on conversation and memory instead of a documented disclosure workflow.

When a dispute starts, “we discussed it” is weak protection. A clear disclosure statement, delivered at the right time and preserved in the file, is much stronger.

What Is a Disclosure Statement at Its Core

A disclosure statement is a formal transparency document. Its core job is to provide all material facts and information that could reasonably affect a person's decision or understanding of a matter. In practice, that includes things like conflicts of interest, risks, and financial information that could change how someone evaluates a transaction or relationship, as explained in this legal definition of a disclosure statement.

The easiest way to think about it is this. A disclosure statement is the document that answers the question, “What would matter to a reasonable person before they move forward?” If the answer could influence consent, price, strategy, or trust, it likely belongs in the disclosure.

Material facts are the center of the document

Not every fact is material. Good disclosure practice separates background noise from decision-grade information.

A useful working test is simple:

- Would this change the person's decision?

- Would this change the terms they would accept?

- Would this change how they evaluate the risk?

If the answer is yes, the fact belongs in the disclosure.

That's why these documents matter in both legal and business settings. They aren't there to bury the other side in paper. They're there to make hidden information visible before that hidden information turns into a dispute.

Practical rule: If a fact would look important later in a deposition, complaint, or fee dispute, treat it as a candidate for disclosure now.

Why the definition matters to your firm

Managing partners don't need another abstract compliance concept. They need a way to reduce preventable conflict. A disclosure statement helps do that because it converts assumptions into documented notice.

That also connects to diligence. If your team is reviewing a deal, onboarding a client, or validating a risk profile, the same discipline applies: identify what matters, confirm it, and document it clearly. For a broader companion read on that mindset, this essential due diligence guide is a useful reference.

A weak disclosure statement reads like paperwork. A strong one reads like a professional record of informed transparency.

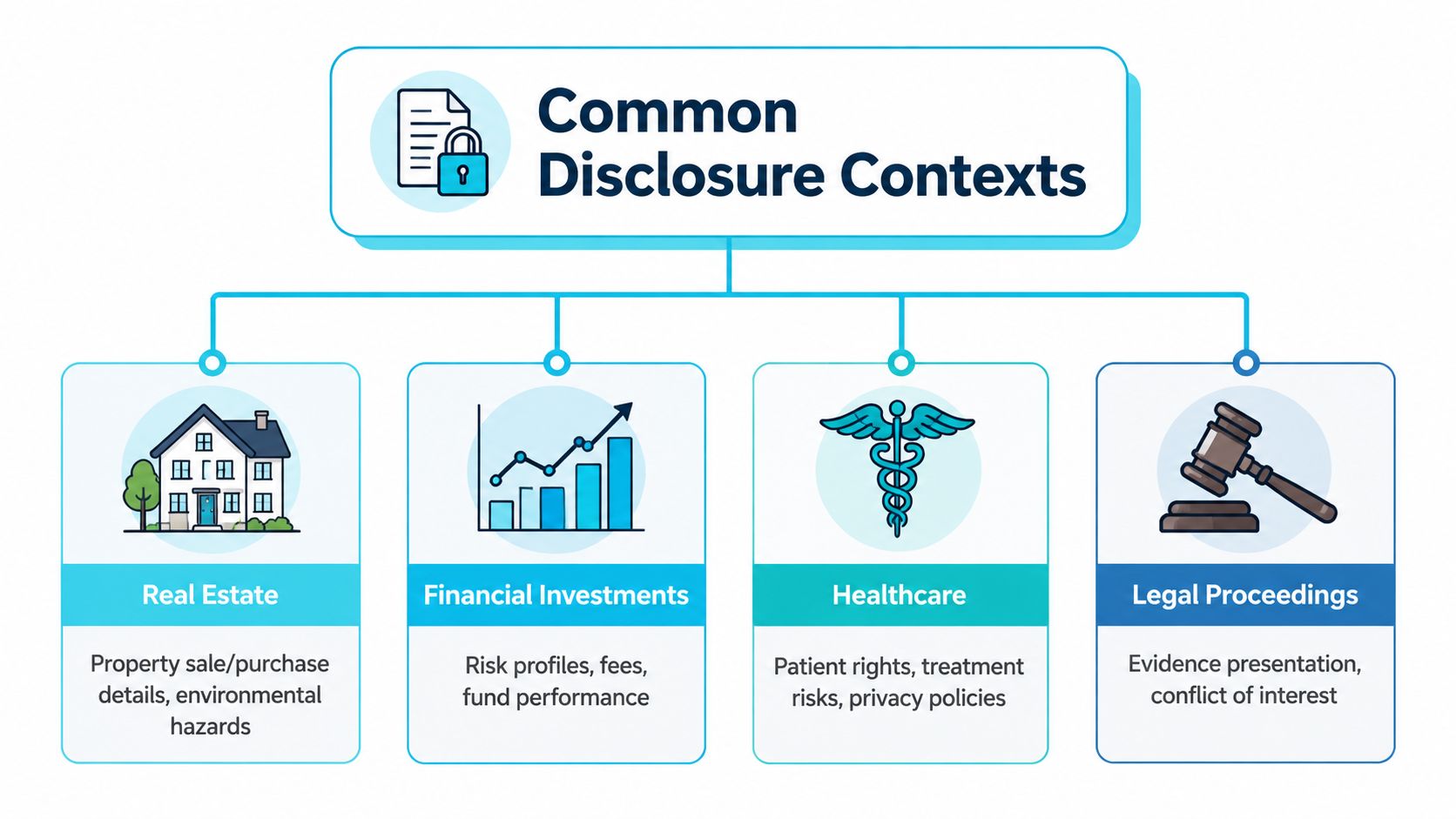

Common Legal and Financial Contexts for Disclosures

Disclosure statements show up in many forms, but they serve the same basic function. They convert hidden or unevenly held information into something another party can use. Outside bankruptcy, they act as risk-allocation tools in areas such as real estate, lending, and securities by turning asymmetric information into decision-grade information for non-expert counterparties, as outlined in this overview of disclosure statements across legal and financial contexts.

Real estate disclosures

Real estate is where many clients intuitively understand disclosure risk. Sellers are typically expected to disclose known material defects such as electrical issues, water damage, environmental hazards, title defects, or structural problems.

That matters because the document changes the legal posture of the transaction. Without clear disclosure, a buyer can later claim they made the purchase without knowing a material fact. With clear disclosure, the seller has a stronger record that the issue was raised before closing.

For law firms, the operational lesson is straightforward. Property disclosures aren't just forms to circulate. They need version control, timing discipline, and proof that the correct party received the final document.

Securities and financing disclosures

In securities and financing matters, disclosure does different work but follows the same principle. Investors, lenders, and counterparties need enough information to evaluate business risks, obligations, conflicts, and pricing.

Firms often underestimate clarity in these situations. Lawyers may understand the term sheet or offering language, but a non-expert recipient often doesn't. A usable disclosure translates legal complexity into informed consent. It doesn't abandon precision. It makes precision understandable.

Attorney client and law firm disclosures

Law firms also create disclosure obligations inside their own client relationships. Fee structures, conflicts, responsibilities, consent issues, and scope limits all involve disclosure logic even when the document isn't labeled a disclosure statement.

A conflict disclosure is a good example. The goal isn't just to satisfy an ethics checkbox. The goal is to put the client in a position to understand the relationship and make an informed choice. If your team needs examples of how conflict issues are commonly framed, Learniverse's guide to conflict offers practical context.

Related documents often sit nearby. Engagement letters, waivers, and consent forms can carry disclosure functions even when they are framed differently. That's one reason firms should treat disclosure management as part of the same operational system used for letters of engagement.

Settlements and legal proceedings

Settlement-related disclosures are often less standardized, but the risk is high. A party needs to understand the consequences of acceptance, including what rights are released, what obligations survive, and how money will move.

In litigation, disclosure can also relate to procedural obligations rather than deal terms. The common trap is assuming that a fact known internally has been adequately disclosed externally. Courts don't credit assumptions. They look at what was provided and whether the process complied with the governing rules.

| Context | Who usually prepares it | Who relies on it | Main purpose |

|---|---|---|---|

| Real estate | Seller and counsel | Buyer, agents, lenders | Reveal known material property issues |

| Securities or lending | Issuer, borrower, counsel | Investors, lenders, counterparties | Explain risk, obligations, and key terms |

| Attorney client matters | Law firm | Client | Clarify fees, conflicts, and scope |

| Settlements and proceedings | Counsel and parties | Client, opposing party, court | Support informed consent and procedural compliance |

The Essential Components and Timing of a Disclosure

A disclosure statement works only when content and timing line up. A perfect document sent too late is often not perfect at all. A timely document with missing assumptions creates the same problem from the opposite direction.

Chapter 11 makes that standard unusually clear. Under 11 U.S.C. § 1125, a disclosure statement must contain “adequate information”, meaning enough information for a hypothetical reasonable investor or creditor to make an informed judgment about the plan. If it's too sparse or leaves out material assumptions, the court can refuse approval, which blocks solicitation of votes and can derail plan confirmation, as described in this Chapter 11 disclosure statement discussion.

What has to be included

The right contents depend on the matter, but the framework is consistent. A sound disclosure statement usually addresses the facts a reasonable person would need before deciding.

That often includes:

- Material risks: What could go wrong, what is uncertain, and what assumptions the recipient is being asked to accept.

- Conflicts or interests: Any relationship, incentive, or divided loyalty that could affect judgment.

- Financial impact: Costs, obligations, exposure, payment structure, or other economic facts.

- Limits and contingencies: Conditions, exceptions, unresolved issues, and dependencies.

- Consequences of proceeding: What the recipient gives up, takes on, or cannot later claim not to know.

The drafting mistake I see most often is omission by familiarity. The team knows the matter so well that it stops noticing what a fresh reader would need spelled out.

When it must be delivered

Timing is where firms create avoidable exposure. A disclosure statement should arrive early enough for the recipient to use it in a real decision, not after practical momentum has already eliminated meaningful choice.

That means the right question isn't “Was it sent?” It's “Was it sent in time for informed judgment?”

A disclosure delivered after the client has mentally committed is often a record of process failure, not proof of informed consent.

This timing issue isn't limited to bankruptcy. The same operational pressure applies in intake, conflicts, settlements, property matters, and financing work. If your firm manages cross-border matters or varied regulatory demands, broad global compliance guidelines can help frame how timing and documentation interact across workflows.

How it should be presented

Format matters because readability affects whether disclosure functions.

Use a practical checklist:

- Put critical facts in the main body rather than burying them in exhibits.

- Use plain language where possible so a non-specialist can understand the implication.

- Separate assumptions from facts so the recipient can see what is known and what is projected.

- Capture acknowledgment when the matter carries meaningful legal or financial risk.

Clear structure doesn't weaken legal precision. It strengthens enforceability because it's easier to show that the recipient had a fair opportunity to understand what mattered.

The High Cost of Inadequate Disclosure

The cost of a bad disclosure rarely appears on the day the document goes out. It appears later, when the firm needs to enforce a position, defend a transaction, or prove the client had enough information to make a valid decision.

That's why inadequate disclosure should be treated as a risk management failure, not a drafting imperfection.

Legal consequences that hit the file

In litigation, failing to provide required initial disclosures can lead a court to exclude that information at trial, potentially harming a party's case. In real estate, seller disclosures can reduce post-sale liability if issues were previously disclosed, which makes timing and completeness as important as content, according to this consumer guide on seller disclosures and related risk.

Those outcomes are materially different, but the lesson is the same. Missing disclosures weaken your position at the exact moment you need the record to hold.

- Evidence can be limited: Information you planned to use may not come in.

- Claims get harder to defend: A party can frame the dispute as concealment rather than misunderstanding.

- Deals become unstable: A transaction that looked finished can reopen through allegations of nondisclosure.

Operational consequences inside the firm

The legal risk is only part of the problem. The internal cost is often what managing partners feel first.

A weak disclosure process creates:

- More partner escalations: Routine confusion becomes leadership work.

- More staff rework: Teams search inboxes, call logs, and draft folders for proof.

- More friction with clients: Even small misunderstandings feel personal when money or rights are involved.

- More exposure to inconsistency: Different practice groups handle similar disclosures differently, which creates uneven risk.

If your firm can't quickly show what was disclosed, when it was disclosed, and who received it, you don't have a disclosure system. You have scattered communications.

Reputational damage is harder to repair

Clients usually won't distinguish between a legal failure and a communication failure. They experience both as a breach of trust. That response can shape reviews, referrals, and future resistance during the matter itself.

A firm can do strong legal work and still lose confidence because the record of transparency feels thin. That's why disclosure discipline belongs in operations, not just doctrine. The prevention work is quiet, but the absence of it is loud.

Modernizing How Your Firm Manages Disclosures

Disclosure statements have become a specific compliance mechanism across sectors, and in financial reporting the U.S. market expectation is that a financial statement without disclosures is unreliable because it lacks the context needed for interpretation, as noted in this discussion of financial statement disclosure requirements and practice. Law firms should take the same operational lesson. A disclosure isn't just content. It's context plus delivery plus proof.

The old workflow is fragile. Staff generate a PDF, email it, save a copy somewhere in the matter file, and hope the client opens it, reads it, and responds. If a dispute later arises, the firm may have the document but not a clean record of delivery, review, follow-up, or acknowledgment.

What a modern workflow should do

A workable disclosure system for a law firm should handle four jobs without creating another administrative burden.

| Need | Old method | Better method |

|---|---|---|

| Delivery | Email with attachment | Secure portal delivery tied to the matter |

| Tracking | Manual notes | Timestamped activity record |

| Intake of responses | Separate forms or phone call | Fillable forms in the same workflow |

| Follow-up | Staff reminders on calendars | Automated reminders and standardized next steps |

That's where a client portal becomes practical rather than cosmetic. A portal can centralize the disclosure statement, related forms, acknowledgments, and follow-ups in one place instead of scattering them across inboxes and drives.

How this helps legal operations

For firms using systems like Needles, Neos, LawBase, or Litify, the best setup is one that supports disclosure management without forcing staff to live in a separate communication tool all day. That reduces friction, which is usually the deciding factor in whether a process sticks.

One option is CasePulse document automation workflows. CasePulse provides a secure client portal for law firms, integrates with case management systems including Needles, Neos, LawBase, and Litify, and allows clients to share files and complete fillable forms while staff continue working in their existing systems. In disclosure-heavy workflows, that kind of setup can support secure delivery, document collection, and a cleaner audit trail around client communications.

What works and what doesn't

What works:

- Single source of truth: The current disclosure and related acknowledgments live in one matter-linked location.

- Standardized templates: Teams don't reinvent language each time.

- Automated reminders: Clients get nudged without staff chasing every response manually.

- Visible ownership: Someone is responsible for issuing, updating, and closing the loop.

What doesn't:

- Inbox-only delivery: Important notices disappear in crowded email threads.

- Local draft chaos: Different versions circulate with no confidence about which was final.

- Verbal supplements without record: Critical explanation happens on a call and never gets memorialized.

- Unowned process: Everyone assumes someone else handled it.

The point isn't to turn every communication into a formal event. The point is to reserve rigor for communications that carry legal, financial, or ethical significance, then manage them in a way the firm can prove later.

Making Transparency Your Strategic Advantage

A disclosure statement is easy to underestimate because it often looks like routine paperwork. It isn't. It's the document that turns hidden facts into informed decisions and informal explanation into a defensible record.

For law firms, that means the issue isn't just knowing what a disclosure statement is. It's building a process that makes disclosure timely, complete, understandable, and traceable. That's where firms separate themselves. Not in theory, but in execution.

The strongest firms treat disclosure as part of client service and risk control at the same time. They don't wait for a dispute to discover that key facts were spread across calls, emails, and attachments. They define ownership, standardize language, deliver documents in a controlled way, and preserve proof.

Good disclosure practice does more than prevent problems. It signals that the firm is organized, candid, and serious about informed client decisions.

That reputation matters. Clients trust firms that communicate clearly. Courts and counterparties respond better to records that show discipline. Staff perform better when they aren't rebuilding the file after the fact.

Transparency, handled well, becomes an operational advantage. It reduces friction, strengthens compliance, and protects the firm when memories differ.

If your firm wants a cleaner way to deliver disclosure-related documents, collect responses, and keep communication tied to the matter record, take a look at CasePulse. It's a secure client portal built for law firms that need clients to message the team, share files, and complete forms without forcing staff out of their existing case management workflow.