Form SS-4 is the IRS application used to obtain an Employer Identification Number, or EIN, and an EIN is a 9-digit number used for tax filing and reporting purposes. In a law firm, that usually means Form SS-4 is one of the first practical documents you deal with when a new entity, estate, or trust needs to function operationally.

If you're handling entity formation, probate administration, trust setup, or the firm's own back office, this form shows up sooner than most new hires expect. It looks administrative, but it affects banking, tax registration, payroll setup, and how cleanly the matter file moves from legal work into operations.

In practice, the biggest mistakes aren't dramatic. They're small. A name doesn't match the formation document. The wrong person gets listed. Someone reapplies when an update would have been enough. Those errors create unnecessary cleanup, and cleanup usually lands on the paralegal, office manager, or firm administrator.

The Foundation of a New Legal Entity

At 4:30 p.m., a client signs the trust, wants the bank account opened the same day, and the file stops because no one addressed the EIN. In a law firm, that delay is rarely a legal problem. It is an operations problem caused by treating Form SS-4 too late in the matter lifecycle.

A new PLLC for the firm, an estate opened in probate, and a settlement trust funded after resolution all reach the same administrative checkpoint. The entity cannot function cleanly until it has its own IRS tax identity tied to the correct legal name, responsible party, and filing status. In practice, that means SS-4 belongs in the setup workflow as soon as the organizing documents are being drafted, not after the client is waiting at the bank or the accountant is asking for tax details.

Inside a firm, this is one of the forms that separates legal formation from actual administration. Articles, certificates, trust instruments, and probate orders create the entity on paper. SS-4 helps the file move into the practical sphere, where someone needs to open an account, issue tax reporting, set up payroll, receive funds, or hand complete records to a financial institution.

That is why experienced staff treat SS-4 as part of intake and implementation, not as clerical cleanup.

The practical risk is not usually a rejection. It is mismatch. If the entity name on the SS-4 does not match the filed formation document, if the wrong person is listed as the responsible party, or if the team files before the ownership and tax classification are settled, the matter turns into avoidable correction work. That correction work usually lands on the paralegal, probate clerk, or firm administrator who has to fix banking paperwork, update the tax file, and explain the delay to the client.

Entity choice also affects how the form should be handled and what downstream administration will look like. For teams advising founders or setting up the firm's own structure, a plain-language resource on understanding business structures can help frame those decisions early. If the filing is part of the firm's own launch checklist, this guide on how to open a law firm fits naturally into the same operations planning.

Who Needs an EIN and When to File Form SS-4

In a firm setting, the question usually isn't "what is Form SS-4" after the first time you see it. The operative question is when the need becomes active. That timing matters because clients often assume the legal document alone is enough. It usually isn't.

The cleanest way to spot the trigger is to ask whether the entity now needs its own tax identity for administration. If the answer is yes, SS-4 moves from optional background task to immediate filing item.

Common law firm triggers

Some triggers come from the firm's own operations:

- New firm entity formation: If the practice is being organized as a corporation, partnership, or other separate entity, you'll usually need to get the EIN process underway early so banking and tax registration don't lag behind.

- Hiring staff: Once the firm is setting up payroll or employment tax reporting, the EIN becomes part of routine administrative setup.

- Structural changes: If the firm changes legal structure, don't assume the old records and the new entity setup can be handled informally. Review the event closely before deciding whether a fresh filing is appropriate.

Other triggers arise in client matters:

- Probate administration: An estate may need its own EIN so administration can proceed under the estate's tax identity rather than an individual's.

- Trust administration: Settlement trusts, special needs trusts, and other client trust arrangements often require separate handling.

- New client business entities: If your firm forms an LLC or corporation for a client, SS-4 often becomes part of the opening deliverables, not an afterthought.

Firm work versus client work

This distinction trips up new staff. The firm may prepare the filing, but the EIN belongs to the entity, not to the law firm handling the matter. That affects naming, responsible party analysis, document retention, and who should keep the confirmation records.

A good internal checkpoint is to ask three questions:

- Whose entity is this?

- Who controls it?

- Where will the official records live after filing?

If your team can't answer those cleanly, the SS-4 probably isn't ready to submit.

The form may be short, but the decisions behind it are matter specific. A trust file, an estate file, and a new PLLC file shouldn't be treated as interchangeable.

State compliance also affects timing. If you're helping with a new LLC in a jurisdiction with its own filing and maintenance requirements, something like this overview of understanding Florida LLC compliance can help staff connect federal EIN work with state level obligations. Internally, firms also benefit from treating this as part of broader operations discipline rather than isolated admin work, which is why it fits with thinking about the law firm as a business.

Navigating Key Fields on Form SS-4 for Law Firms

A file opens at 4:30 p.m. The corporate client needs an EIN for a new subsidiary before the bank will finish onboarding, and the estate team is also waiting on an EIN for a probate matter. In both files, the form is short. The risk sits in the same places every time: name, responsible party, entity classification, and reason for applying.

Legal name means the name in the governing record

Use the exact legal name from the document that created or governs the entity. For a new LLC or corporation, that usually means the filed formation document. For an estate, trust, or settlement trust, it means the probate papers, trust instrument, or court order that names the entity.

Internal shorthand causes avoidable cleanup work. A matter may be labeled "Doe Family Trust" in the DMS, but if the signed instrument says "The John A. Doe Irrevocable Trust dated March 3, 2024," that is the name staff should carry onto the SS-4. Banks, payroll providers, and accountants compare documents closely, and minor differences in wording, punctuation, or dates can slow the next step in the file.

The safest office practice is simple:

- Pull the name from the source document, not the matter nickname

- Match punctuation, initials, dates, and trust titles exactly

- Save the supporting document with the filed SS-4 copy

That last step matters inside a law firm. If bookkeeping, tax, or probate staff touch the file later, they should be able to see why the name was entered that way without asking the original drafter.

The responsible party field needs a legal and practical check

Law firm staff often get this wrong for understandable reasons. The attorney signs engagement letters, paralegals assemble the filing packet, and firm administrators track deadlines. None of that makes the firm the responsible party.

The answer depends on who controls or administers the entity. In a business formation matter, that may be the owner or principal. In an estate, it may be the executor or personal representative. In a trust matter, it may be the trustee. Listing the attorney or the law firm because the firm prepared the SS-4 creates confusion later, especially if the IRS, a bank, or an accountant expects the listed person to have authority.

I train staff to stop and answer one question in writing: Why is this individual the responsible party for this entity? If the file cannot support that answer with the governing documents or attorney confirmation, the form is not ready.

Entity type and reason for applying should match the matter, not the template

Template use saves time, but it also creates repeat errors. A business formation template can push staff toward business-oriented answers even when the file is an estate or trust administration matter. That is how firms end up with an SS-4 that technically submits but does not match the actual file.

Match each key field to a document or event already in the matter:

| Field | What to confirm | Common law firm error |

|---|---|---|

| Legal name | Filed formation document, trust instrument, probate order, or other governing record | Using the matter caption or internal shorthand |

| Responsible party | Person with actual authority or administration responsibility | Listing the lawyer, paralegal, or firm name |

| Entity type | The legal structure shown in the file documents | Copying the classification from a prior matter |

| Reason for applying | The real trigger, such as formation, estate administration, trust administration, banking, or hiring | Choosing a box that fits the template rather than the file |

This distinction shows up clearly in client matter management. A new PLLC for a physician client, a decedent's estate, and a settlement trust may all land on the same admin desk, but they should not be processed as if they were the same kind of entity. Good intake notes help. Better document review helps more.

Record the filing decision, not just the form

Saving the submitted SS-4 is not enough. Save the reasoning behind the answers. A short internal note in the matter file prevents avoidable rework when someone asks six months later why a trustee was listed, why a trust name includes a date, or why the EIN was obtained before the bank packet went out.

A useful note can be brief:

- Legal name pulled from the signed governing document or filed entity record.

- Responsible party confirmed by attorney review and supporting file documents.

- Entity type based on the document creating or governing the entity.

- Reason for applying tied to the actual operational need in the matter.

That habit helps both client work and firm operations. If the EIN belongs to a client entity, the matter file should show the authority for each answer. If the filing is for the firm or an internal affiliate, the administrative record should do the same. In either case, clean documentation is what keeps a short federal form from turning into a long cleanup project.

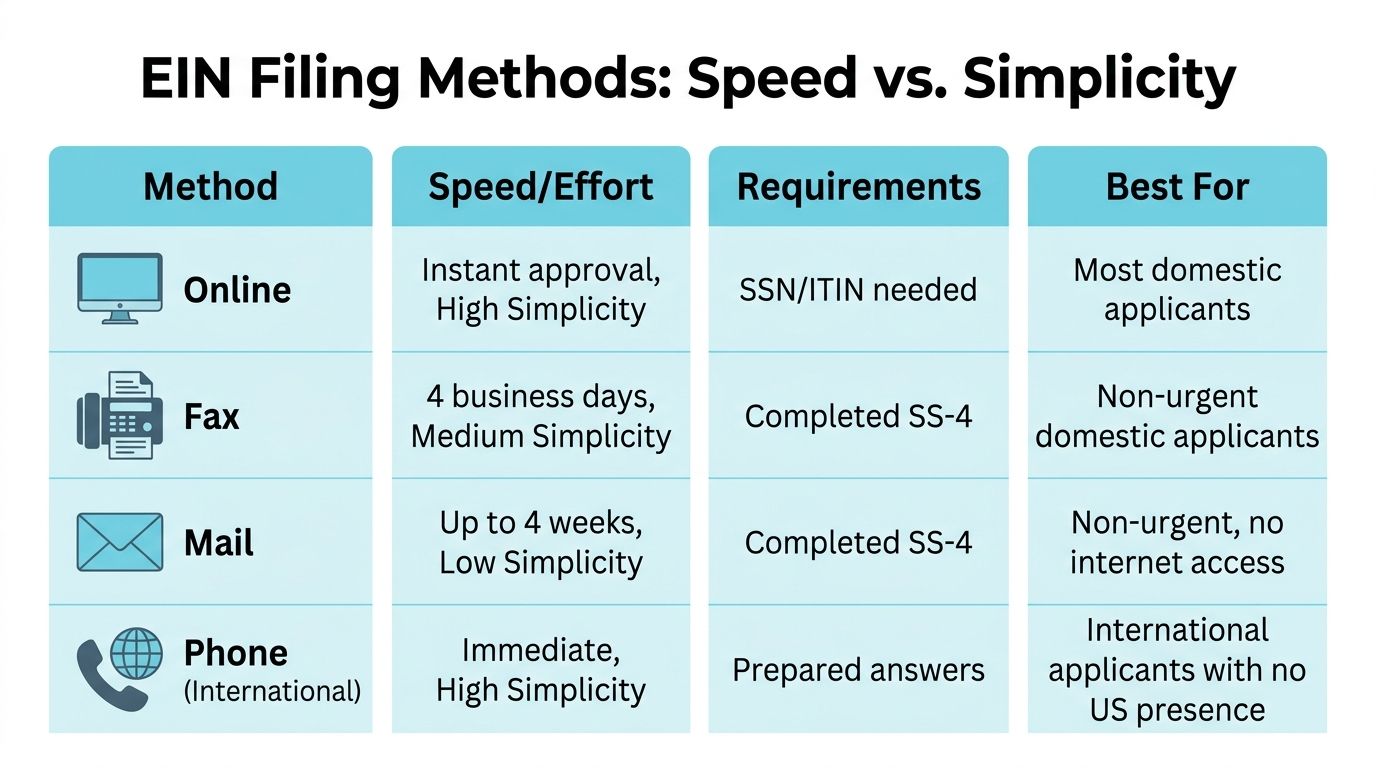

Choosing Your Filing Method Speed vs Simplicity

A partner approves a new client entity at 3:30 p.m. The banking packet is waiting, the accountant wants the EIN before morning, and the matter cannot move until the number is in hand. In a law office, filing method is not an administrative afterthought. It affects whether the rest of the file stays on schedule.

The right choice depends on two things. First, how quickly the EIN is needed for the matter. Second, whether the file is clean enough to support a fast submission without last-minute corrections. For client work, that often means coordinating with the attorney handling the formation, probate, or trust administration. For firm operations, it may mean timing payroll setup, retirement plan administration, or a new bank account for an affiliate.

Form SS-4 filing method comparison

| Method | Processing Time | Confirmation | Best For |

|---|---|---|---|

| Online | Fastest option when the applicant qualifies and the session can be completed in one sitting | Immediate EIN issuance at the end of a successful session | Domestic applicants with time-sensitive banking, tax, payroll, or matter opening needs |

| Fax | Slower than online, but often faster than mail | Written response through the fax process | Files that need quicker handling and benefit from a reviewed PDF record before submission |

| Slowest option | Delayed written response | Matters with no short deadline and no downstream task waiting on the EIN | |

| Phone for international applicants | Used for qualifying international applications | Direct interaction during the call process | International applicants and cross-border matters handled under the IRS phone procedure |

How law firms usually make the call

Online filing is usually the first choice for domestic matters that are fully ready. It works well when the supervising attorney has confirmed the details, the responsible party information is settled, and someone can stay with the submission from start to finish. That last part matters. An interrupted filing session can create its own waste.

Fax works well in offices that build review into the workflow. If the completed SS-4 has already gone through attorney or senior staff signoff, fax gives the team a clear submitted version and a filing path that fits a document-driven process. I have seen this work especially well on trust and estate files where the office wants the exact signed form saved before anything goes out.

Mail still has a place. It is just a deliberate choice, not a default. Use it when the matter has no short operational deadline and no one is waiting to open an account, issue payments, or complete a registration tied to the EIN.

- Choose online for urgent files: best for same-week banking, payroll setup, tax registration, or entity launch tasks.

- Choose fax for reviewed files that need a documented submission path: useful when the office wants approval built into the process.

- Choose mail only when delay will not affect the matter: if another team member is waiting on the EIN, mail usually creates avoidable lag.

One firm habit helps here. Put the target date for the EIN in the matter notes before anyone files. That gives staff a concrete deadline instead of a vague instruction to "get it done soon."

Match the filing method to the downstream task

The filing method should fit what happens next in the file. A new PLLC that needs a bank account this week calls for a different approach than an estate matter where no institution will request the EIN for several weeks. The same is true inside the firm. If accounting needs the number to set up payroll or tax records, speed may matter more than preserving a paper-first routine.

Problems usually start when no one asks that question early enough. The SS-4 gets prepared correctly, then sits in a slower filing channel that does not match the deadline. In practice, that is one of the easiest delays to prevent.

Common Filing Mistakes and How to Avoid Them

At 4:45 p.m., the attorney wants the EIN application filed before close of business so the client can open an account the next morning. That is when bad SS-4 habits show up. In a law firm, the usual problem is not ignorance of the form. It is rushing past the documents and filing from memory, email shorthand, or last week's draft.

The fix is simple. Treat the SS-4 as a controlled filing tied to the matter record, not as stand-alone admin work.

Mistake one: using the wrong legal name

This happens more than staff like to admit. A paralegal copies the entity name from intake notes, a trust name from an unsigned draft, or an estate name from a probate caption that does not match the taxpayer name the IRS needs.

Use the controlling document that governs the filing. For a new entity, that may be the filed formation document. For a trust, it is the executed trust instrument. For an estate, confirm how the estate should be identified based on the probate file and the supervising attorney's instructions. If the final document is not in the file, stop and get confirmation before submitting the SS-4.

A one-word mismatch can turn a same-day task into follow-up with the bank, the accountant, or the IRS.

Mistake two: naming the wrong responsible party

Law firms see this error often in trust, estate, and entity matters because the firm is close to the process. That does not mean the firm should be listed in a role that belongs to the client, trustee, personal representative, member, or other person with actual authority.

The responsible party should match the legal structure and the facts of the file. If the attorney gives direction on who to list, note that decision in the matter record. That protects the file later when a bank compliance team, successor fiduciary, or tax preparer asks why a particular person appears on the application.

Do not let convenience decide the field.

Mistake three: filing a new SS-4 when the file calls for an update

Staff sometimes reapply for an EIN because the address changed, the firm contact changed, or the entity record needs cleanup. That creates duplicate work and can confuse the client file.

In many matters, the core issue is maintenance of the existing tax identification record. Firm administrators should flag these situations for tax follow-up instead of reflexively preparing another SS-4. This is one place where solid law firm bookkeeping procedures help, because the accounting and legal sides of the file need the same taxpayer information to stay aligned.

Mistake four: failing to tie the application to the matter workflow

An SS-4 should not live only in one person's inbox or browser history. In a firm setting, the EIN request affects downstream tasks such as banking, trust administration, payroll setup, client accounting, and tax reporting.

If the preparer files the form but does not save the final version, note the submission date, and identify who requested it, the next person on the file has to reconstruct the history. That is where avoidable errors start.

A review process that catches the common errors

Use a short second review before filing. It does not need to be elaborate, but it should answer the questions that matter:

- Does the legal name match the signed or filed governing document exactly?

- Does the responsible party fit the entity, trust, or estate structure?

- Is this a new EIN event, or does the file call for an update to an existing record?

- Are the supporting documents and final SS-4 saved in the correct matter location?

- Will the next team handling banking, tax, or administration be able to see what was filed and why?

The best firms make one person accountable for this final check. SS-4 errors usually come from handoff gaps, not hard legal analysis. A two-minute review at filing saves far more time than cleaning up a bad EIN record after the client has started using it.

After Filing Next Steps for Firm Administrators

A probate paralegal gets an EIN for an estate on Tuesday. By Friday, the bank is asking for proof, the tax team wants the number for its file, and the attorney assumes the matter record already has the confirmation notice. If the SS-4 result is sitting in one person's email, the office has created a preventable handoff problem.

What to do as soon as the EIN is issued

Treat the EIN confirmation like an operative file document, not a temporary receipt. For a client matter, save it in the matter workspace with the governing document that supported the filing. For the firm's own records, store it where accounting, payroll, and administrative staff can retrieve it without asking who originally filed the SS-4.

Then update the systems that rely on that number.

- Add the EIN to the correct matter or administrative record.

- Save the confirmation notice in a secure, searchable location.

- Alert the team handling banking, tax filings, payroll, or trust administration.

- Document the filing date, filing method, and who submitted it.

That last step matters more than it sounds. In a law office, the person opening the bank account, preparing fiduciary income tax returns, or setting up vendor payments is often not the person who filed the SS-4. Clean records keep those downstream tasks from stalling. Good coordination between the legal file and the accounting file is part of sound law firm bookkeeping.

Keep the EIN record current

An issued EIN is not a closed file item. The related record still needs maintenance if the entity's address changes, the responsible party changes, or the structure changes enough to require an IRS update.

This comes up often in firm practice. A successor trustee steps in. An estate administration shifts to a different mailing address. A client reorganizes an entity after formation. If no one owns the follow-up, the IRS record, the bank record, and the matter file start to diverge, and staff spend billable and nonbillable time figuring out which version is correct.

The practical fix is simple. Add an EIN follow-up checkpoint to your entity, probate, and trust administration closing checklist. If the matter stays open for months or years, review whether any change should be reported rather than assuming the original SS-4 still reflects current facts.

If the original notice is lost

Handle that as a records and verification issue first. Do not assume a missing notice means the office needs a new EIN.

Start with the file. Check the matter management system, the tax folder, prior banking packets, and the accountant's records. If the number was validly issued, the task is usually to recover proof or confirm what was already assigned, not to submit another SS-4 and create a bigger problem.

In practice, that distinction saves time. A duplicate filing can complicate account opening, tax reporting, and internal bookkeeping because staff may start using different taxpayer IDs for the same client entity, trust, or estate.

Frequently Asked Questions About Form SS-4

Is Form SS-4 only for new businesses

No. In law firm practice, it also comes up for estates, trusts, and other entities that need their own tax reporting identity. That's why litigation, probate, estate planning, and firm administration staff may all encounter it.

Should the law firm be the responsible party for a client entity

Not by default. The firm may prepare the form, but that doesn't mean the firm should be inserted into a role that belongs to the person who controls or administers the entity. Confirm the specific facts of the matter before filing.

What if the EIN confirmation letter is lost

Treat that as a records problem first, not as a reason to submit a brand new SS-4. Check the file, check with the accountant or bank if applicable, and determine whether replacement proof is what you need.

If the address or ownership changes, do we file a new SS-4

Not automatically. The IRS says changes to address, ownership, or structure should be reported within 60 days using Form 8822-B. The key is to distinguish an update from a true new EIN event.

What's the best internal policy for handling SS-4s in a law office

Keep a copy of the filed SS-4, the confirmation notice, and the source document that supported the key entries. If another staff member can't open the file later and understand why the form was completed the way it was, the record isn't complete enough.

If your firm wants the administrative side of legal work to feel less fragmented, CasePulse helps centralize client communication, file sharing, forms, and updates inside the systems your staff already uses. That can make it easier to support operational tasks around entity setup, trust administration, and client record management without creating another disconnected inbox for the team.